Blockchain Technology 101 – A Definitive Guide

Blockchain technology is fundamentally transforming how we approach data security, trust, and transparency in the digital world.

It’s an ingenious invention that allows information to be distributed across a network securely without being copied or altered, giving you a new degree of confidence in online transactions.

At its core, blockchain consists of a sequence of blocks, each containing data that is chained to the previous block through complex cryptographic principles, ensuring the integrity of the entire chain.

The versatility of blockchain extends beyond its most famous application, cryptocurrencies like Bitcoin. It also serves as the backbone for a myriad of applications across various sectors, including finance, supply chain management, and even voting systems.

Smart contracts, which are self-executing contracts with the terms directly written into code, are another innovative byproduct of blockchain, opening the doors to decentralized applications (DApps) that run exactly as programmed without any chance of fraud or third-party interference.

Key Takeaways

- Blockchain increases data integrity with its secure, tamper-proof system.

- Its applications span many industries, not just cryptocurrency.

- Innovations like smart contracts leverage blockchain for more efficient operations.

Understanding Blockchain Technology

When you hear about blockchain, it’s likely in the context of it being a revolutionary technology that powers cryptocurrencies like Bitcoin. Here, we’ll break down what blockchain is and why its features like decentralization and immutability are stirring up conversations across various industries.

Defining Blockchain

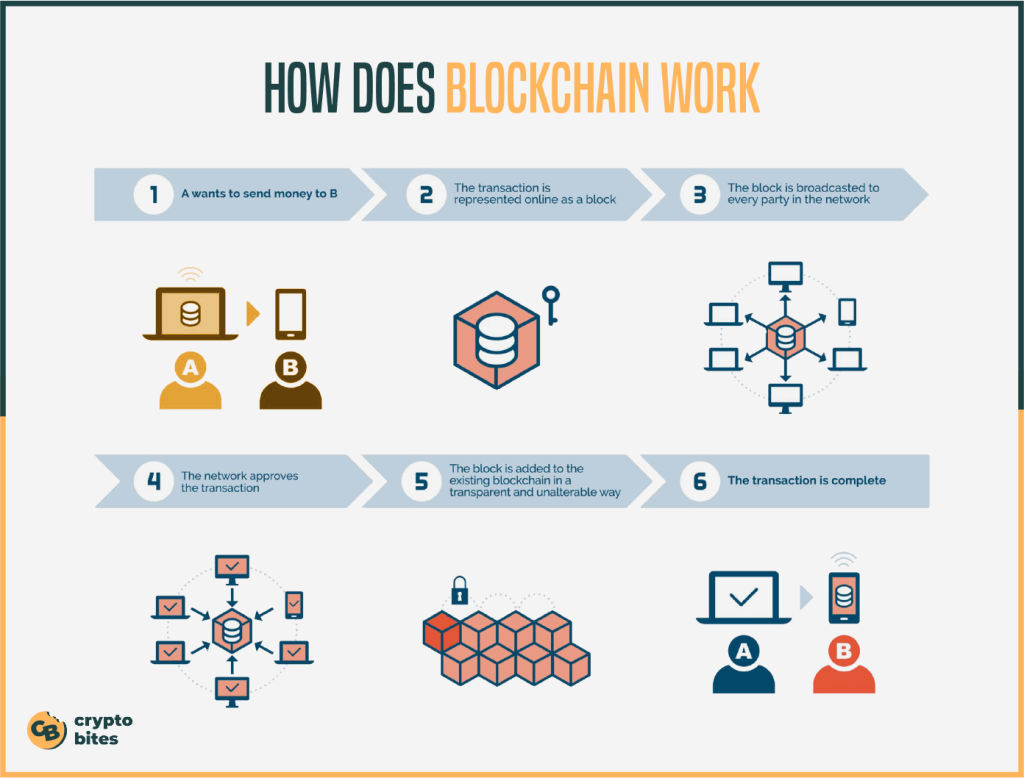

Blockchain serves as a digital ledger that is utilized to record transactions across many computers. The unique aspect of blockchain is that once a transaction is recorded, it becomes nearly impossible to change. This technology supports cryptocurrencies, providing a decentralized network where records, once confirmed, become part of a permanent ledger called the blockchain. A key distinguishing feature of blockchain technology is its immutable nature, which establishes trust in the data it keeps.

Here is a detailed visual of how blockchain works:

Key Features of Blockchain

The key features that define blockchain technology and make it distinct include:

- Decentralized: Unlike traditional ledgers managed by a central authority, blockchain operates on a peer-to-peer network basis, where each participant, or node, has a copy of the ledger, increasing transparency and security.

- Immutable Records: Once data is added to the blockchain, it is extremely difficult to alter. This means that once a transaction is added to the ledger, it’s permanently recorded, establishing an accurate and tamper-resistant history. It makes sharing data on blockchain much secure and reliable.

- Distributed Ledger Technology (DLT): This refers to the shared and synchronized digital data geographically spread across multiple sites, countries, or institutions. No single entity has control over the ledger, which ensures that the records on the blockchain are publicly verifiable and accessible by all network participants.

These properties not only make it an integral part of cryptocurrency systems but also position blockchain as a promising solution for various applications that require untamperable and transparent record-keeping.

How Will Blockchain Change the World?

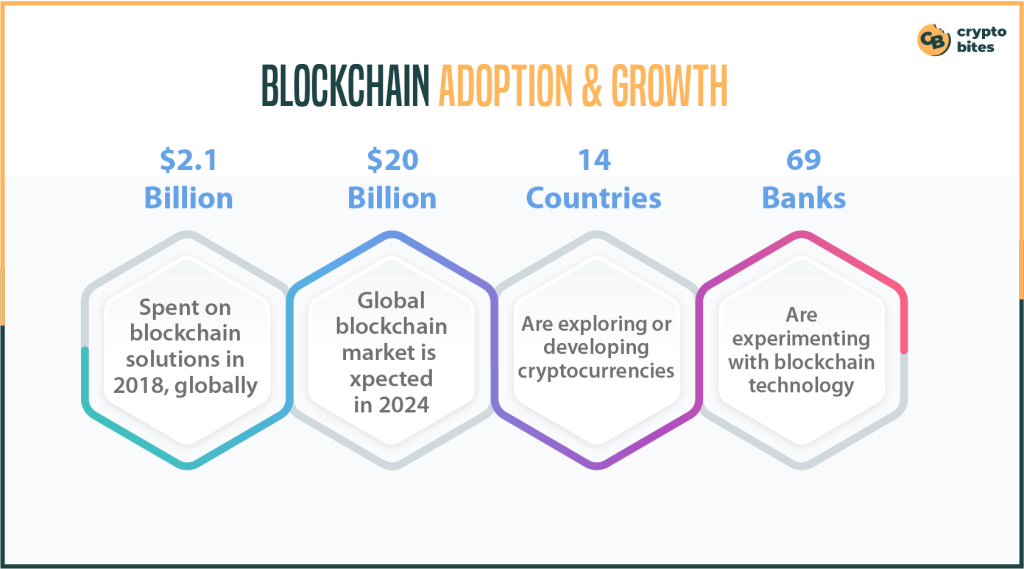

A World Economic Forum report forecasts that by 2025, approximately 10% of the global GDP will be secured through blockchain technology or its derivatives!

Blockchain technology is disrupting industries with its promise of secure, transparent, and efficient transactions. This goes beyond just financial applications – it has the potential to fundamentally change how we operate in everything from food safety to healthcare.

Blockchain creates a decentralized system, where a shared record is constantly monitored by everyone involved. This eliminates the need for intermediaries, reducing costs and building trust. Imagine a world where the organic certification of your avocado or the legitimacy of your online purchase is instantly verifiable. Blockchain ensures this by creating an immutable record, promoting accountability and reducing fraud across entire systems.

But the impact of blockchain reaches further. It has the potential to revolutionize online marketplaces, empowering creators and consumers alike. Additionally, it can secure assets and streamline government operations, all while paving the way for a more transparent and equitable society.

As blockchain continues to evolve and integrate into various sectors, its impact on how we interact, conduct business, and even govern ourselves will be undeniable. The future landscape of technology and business is undoubtedly linked to the ongoing development of blockchain.

Want to dive deeper? Explore more on how blockchain is going to change the world.

The 5 Layers in Blockchain

Blockchain technology is a complex and layered system designed to ensure the secure and transparent transfer of information. These layers work in tandem to create a decentralized and tamper-resistant network.

Here’s an overview of the five fundamental layers within blockchain:

1. Hardware Infrastructure Layer

At the foundation of the blockchain architecture lies the hardware infrastructure layer. This layer comprises the physical components that support the blockchain network, such as servers, nodes, and communication devices. The robustness and reliability of this layer are crucial for the overall stability and performance of the blockchain system.

2. Data Layer

Above the hardware infrastructure is the data layer, which is responsible for managing the storage and organization of data within the blockchain. This layer incorporates the distributed ledger technology, where each participant in the network maintains a copy of the entire blockchain. The data layer ensures that information is stored securely and in a way that is resistant to unauthorized modifications.

3. Network Layer

The network layer facilitates communication and interaction between nodes in the blockchain network. It ensures the seamless transmission of data across the decentralized network, enabling nodes to share information, validate transactions, and synchronize their copies of the blockchain. The network layer plays a crucial role in maintaining the integrity and consistency of the distributed ledger.

4. Consensus Layer

The consensus layer is pivotal for establishing agreement among nodes on the validity of transactions and the state of the blockchain. It dictates the rules by which consensus is achieved, ensuring that all nodes reach a common understanding of the current state of the ledger. Various consensus algorithms, such as Proof of Work (PoW) or Proof of Stake (PoS), are implemented at this layer to validate transactions and secure the network against malicious activities.

5. Application Layer

Finally, the application layer is the outermost layer and the one that users interact with directly. This layer encompasses decentralized applications (dApps) and smart contracts, which leverage the underlying blockchain infrastructure to provide various functionalities. Users can execute transactions, deploy smart contracts, and engage with the decentralized ecosystem through applications built on top of the blockchain.

These five layers collectively form the intricate architecture of a blockchain, with each layer contributing unique functionalities to ensure the security, transparency, and decentralization of the network.

Read more here if you wish to explore blockchain layers in a much more detailed manner.

The Structure of Blockchain

When you delve into blockchain, you’re looking at a highly secure and transparent way to chronicle transactions. At a glance, the elegance of blockchain lies in its blocks, the cryptography securing them, and the chain that binds them together into an immutable ledger.

Blocks and Transactions

Each block in a blockchain contains a compilation of transactions, much like a page in a ledger. After transactions are verified, they are bundled into a block, which is given a unique hash. This hash is crucial as it not only represents the block’s data but also helps secure it. Each block also has a timestamp when it was added to the blockchain, ensuring the sequence of transactions is permanently recorded.

- Block Components:

- Hash: Unique identifier

- Timestamp: Date and time of creation

- Transactions: List of transactions included

The Chain and Its Integrity

The integrity of a blockchain stems from its structure; imagine it as a series of blocks linked together into a chain. Every new block includes the previous block’s hash, creating a chain that ties every block to its predecessor and making the ledger immutable. This design ensures that once data is recorded, it cannot be altered without changing every subsequent block, which is computationally infeasible.

Cryptography in Blockchain

Cryptography is what keeps your transactions secure on the blockchain. It’s not just about creating complex puzzles; it’s about ensuring that each transaction can be traced to its source without any chance of forgery. Cryptographic algorithms generate the hashes that protect each block, verify the integrity of the data, and maintain the trust in the system’s immutable ledger.

- Cryptography Concepts:

- Hash Functions: Creates a unique hash for each block

- Digital Signatures: Confirms the authenticity of a transaction

Blockchain Network Platforms and Cryptocurrency

Blockchain networks are the underlying technology that enable cryptocurrencies like Bitcoin, Ethereum, and Litecoin to operate securely and transparently. You’ll discover that these decentralized systems have changed the way we think about digital currency.

Bitcoin and Its Mechanism

Bitcoin, the first cryptocurrency, introduced the world to the concept of a decentralized digital currency. Its blockchain operates as a public ledger for all transactions, secured with a proof-of-work mechanism. Each transaction is verified by network nodes and recorded in a block. Once confirmed, blocks are added to the blockchain, creating a robust and tamper-resistant record.

Ethereum Platform

The Ethereum platform goes beyond just digital currency. It allows for the creation of decentralized applications (dApps) through smart contracts, which are self-executing contracts with the terms of the agreement directly written into code. While Ethereum possesses its own currency, called Ether, its principal innovation lies in these programmable contracts that automate transactions and applications.

Other Cryptocurrencies

Beyond Bitcoin and Ethereum, numerous other cryptocurrencies exist, each with unique features. Litecoin, for example, was designed to process transactions more quickly. These digital currencies form an ever-expanding ecosystem, leveraging blockchain technology to fulfill diverse roles, like privacy coins or utility tokens for specific blockchain applications.

Blockchain Security

As you explore the realm of blockchain technology, it’s crucial to understand that blockchain security encompasses various mechanisms designed to protect network integrity and users’ assets.

Security Mechanisms

Blockchain security is built on the robustness of cryptography. Your transactions and data are safeguarded by complex algorithms that create a secure and immutable record.

- Encryption: Ensures that your information is stored in a form that is unreadable to anyone without the correct key.

- Public/Private Keys: A pair of cryptographic keys that enable you to perform secure transactions on the blockchain.

The consensus models, such as Proof of Work or Proof of Stake, are pivotal to maintaining the decentralized integrity of the blockchain. They ensure that all participants agree on the true state of the blockchain ledger.

Potential Vulnerabilities

Despite the inherent security features, blockchain isn’t impervious to threats:

- 51% Attack: This happens if a user or group gains control of more than 50% of the network’s mining power, allowing them to disrupt the network by double-spending coins and halting new transactions.

- Vulnerabilities: Just like any technology, blockchain can have vulnerabilities in its implementation that could potentially be exploited by malicious actors.

Your awareness of these risks helps in appreciating the measures taken to fortify blockchain security and the ongoing efforts to address vulnerabilities.

Types of Blockchain

Blockchain technology has evolved to accommodate various needs, offering diverse solutions tailored to specific requirements. Let’s find out the three distinct types of blockchains, each designed to address specific use cases and preferences:

1. Public Blockchain

A public blockchain operates in the open domain, allowing unrestricted participation from anyone without limitations. This decentralized network is governed by consensus algorithms or predefined rules.

Public blockchains are commonly associated with cryptocurrencies, exemplified by Bitcoin and Ethereum. Participants, known as nodes, contribute to the validation and verification of transactions, ensuring the integrity and security of the network.

The transparency and inclusivity of public blockchains make them suitable for applications requiring a trustless and borderless environment.

2. Private or Permissioned Blockchain

In a private or permissioned blockchain, organizations have granular control over access to the blockchain data. Unlike public blockchains, entry is restricted, and specific permissions determine who can view or participate in the network.

This type of blockchain is ideal for scenarios where privacy, confidentiality, and regulatory compliance are paramount.

The Oracle Blockchain Platform, for instance, uses a permissioned blockchain to provide businesses with a secure and customizable environment, enabling controlled access to sensitive information and transactions.

Public and private blockchains share similarities but also possess significant differences. If you’re interested in delving into the key areas of distinction between the two, I recommend you go through our blog on the key differences between public and private blockchains.

3. Hybrid Blockchain

A hybrid blockchain is a blockchain system that merges features from both public and private blockchains. By blending the strengths of each type, it creates a versatile network capable of safeguarding data and transactions effectively. In a hybrid blockchain, elements of public accessibility coexist with the privacy and control inherent in private blockchains.

Here are some of the key takeaways of a hybrid blockchain:

- Combines Public and Private Elements: A hybrid blockchain integrates features from both public and private blockchain architectures.

- Preserves Data Privacy: Private data remains within the network while ensuring transaction verifiability and integrity.

- Immutable Transactions: Transactions on the private segment of the blockchain cannot be altered, enhancing security.

- Enhanced Business Options: Businesses can establish permission-based networks alongside public ones, expanding blockchain implementation possibilities.

- Coexistence of Public and Private Entries: Both public and private entries coexist within the hybrid blockchain’s database.

- Public Nodes: Operate similarly to those in public blockchains, allowing anyone to join and contribute to the network.

- Private Nodes: Managed by specific entities or individuals, responsible for validating and scrutinizing transactions.

- Faster and More Secure Transactions: Utilizing private nodes can lead to faster, more secure, and more private transactions.

4. Consortium or Federated Blockchain

A consortia or federated blockchain involves a network where a predefined group of stakeholders or nodes closely oversees the consensus process, commonly known as the mining process. This collaborative approach strikes a balance between decentralization and control.

Consortium members collectively validate transactions, enhancing efficiency while maintaining a level of trust among participants. Such blockchains find applications in industries where multiple entities collaborate, such as supply chain management or financial consortia.

The federated structure ensures a degree of governance and cooperation among the involved parties, fostering a shared and secure blockchain ecosystem.

While hybrid and consortium blockchain may sound exactly similar, there however, are some differences. Check out this blog to learn more about the key points of differences between consortium and hybrid blockchains.

What Sets Blockchain Apart from Conventional Record Keeping?

Blockchain differs from traditional database models in several key ways:

- Immutability:

- Traditional Database: Data can be easily tampered with by individuals who have access to it.

- Blockchain: Decentralized records on a blockchain make it practically impossible for anyone to tamper with data, ensuring its integrity.

- Security:

- Traditional Database: Centralized servers are vulnerable to malicious attacks, as seen in incidents like the Equifax data leaks.

- Blockchain: Decentralization in blockchain significantly raises the difficulty of attacks, as hackers would need to compromise every node on the network simultaneously, making it more secure.

- Redundancy:

- Traditional Database: Data is stored in a centralized location, posing a risk of loss in case of damage or server downtime.

- Blockchain: Identical sets of data are distributed worldwide, providing redundancy and resilience in the face of data damage or server issues.

- Cost/Overhead Reduction:

- Traditional Database: Centralized systems may incur higher costs for maintenance and security measures.

- Blockchain: The decentralized nature of blockchain reduces the overhead costs associated with maintaining centralized servers.

- Accountability/Transparency:

- Traditional Database: Limited transparency in centralized systems, making it challenging to ensure accountability.

- Blockchain: Offers transparency by allowing all participants to have a copy of the same data, promoting accountability and trust among users.

These, however, are not the only reasons. There are plenty more reasons as to why you would choose blockchain over conventional record-keeping mechanisms and you can find it all here.

Benefits of Blockchain

Blockchain would not have become such a popular technology if it did not offer so many benefits. Here are some of the key reasons why people prefer blockchain:

1. Pseudoanonymity

Provides a level of anonymity in transactions, though achieving complete anonymity is challenging. Users can conduct transactions using public keys, contributing to a sense of privacy. Blockchain is an ideal system for those who value privacy as it has numbers of different security mechanisms that makes it way stronger than other systems of data movement.

2. Traceability

Transactions on the blockchain are traceable back to public keys, fostering transparency and accountability. This feature is crucial for tracking financial activities and preventing fraudulent transactions.

3. Global Connectivity

Facilitates an anonymous, free, and instant payment system that connects users worldwide. This global connectivity eliminates barriers in traditional financial systems.

4. Security

The decentralized and distributed nature of blockchain enhances the security of financial transactions. Unlike centralized systems, blockchain’s structure makes it more resilient to malicious attacks.

5. Potential for Privacy

While maintaining full anonymity is challenging, certain practices, such as mining anonymously, engaging in peer-to-peer transactions, and using VPNs, can contribute to increased privacy for users.

6. Long-Term Perspective

Reflects curiosity about the long-term value of blockchain-based assets like cryptocurrencies (e.g., moons) over centuries. This interest highlights the evolving nature of blockchain technologies and their potential impact on the financial landscape.

While these are indeed some of the key benefits, exploring our blog will reveal numerous other impressive advantages of blockchain technology that are sure to amaze you!

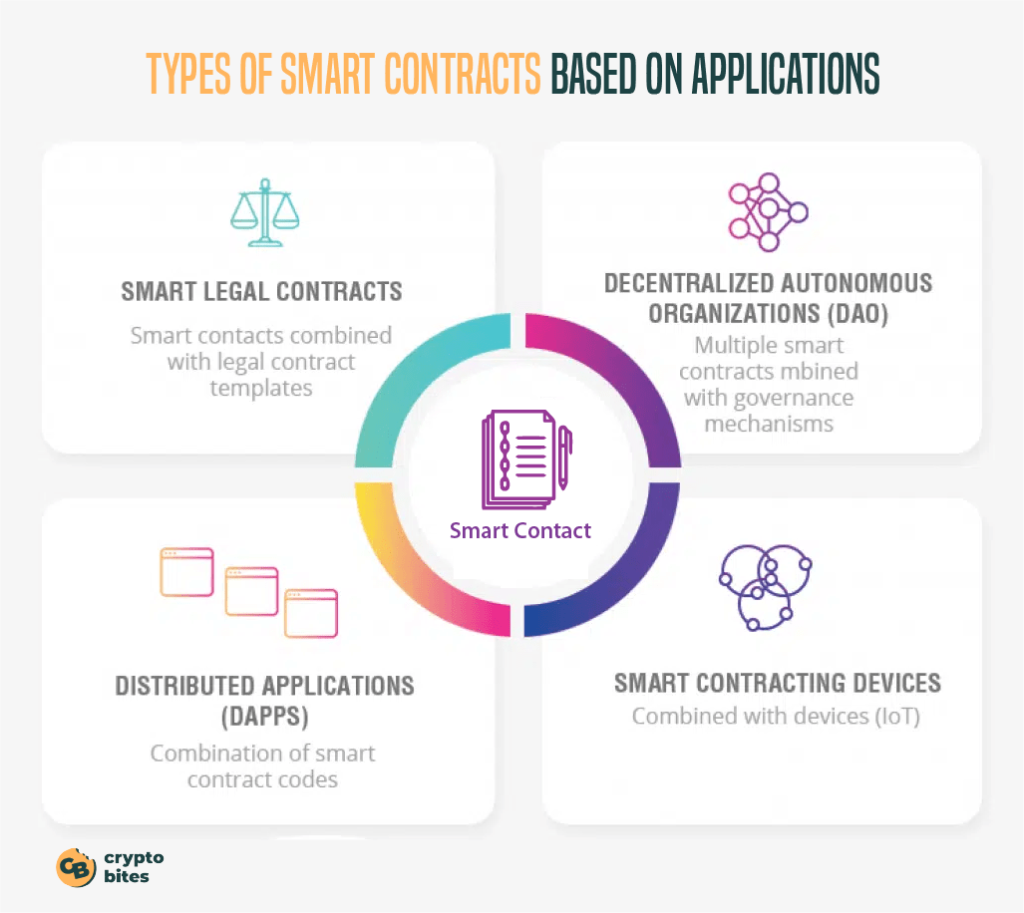

Smart Contracts and DApps

Within the realm of blockchain technology, smart contracts and decentralized applications (DApps) stand out as revolutionary tools. These allow you to interact with the blockchain in ways that are secure, transparent, and without the need for a middleman.

Implementing Smart Contracts

To implement smart contracts on blockchain platforms like Ethereum, you begin by writing self-executing contracts in code. Imagine these as digital agreements that automatically enact and verify a contract’s terms. Thanks to Ethereum’s support, smart contracts uphold immutability, which means once they’re deployed, their terms cannot be changed. They work as programmed, every time, thus cultivating trust in the following way:

- Transparency: Every action taken by the smart contract is visible on the blockchain.

- Security: Immutability prevents tampering, as the terms are set in stone once live.

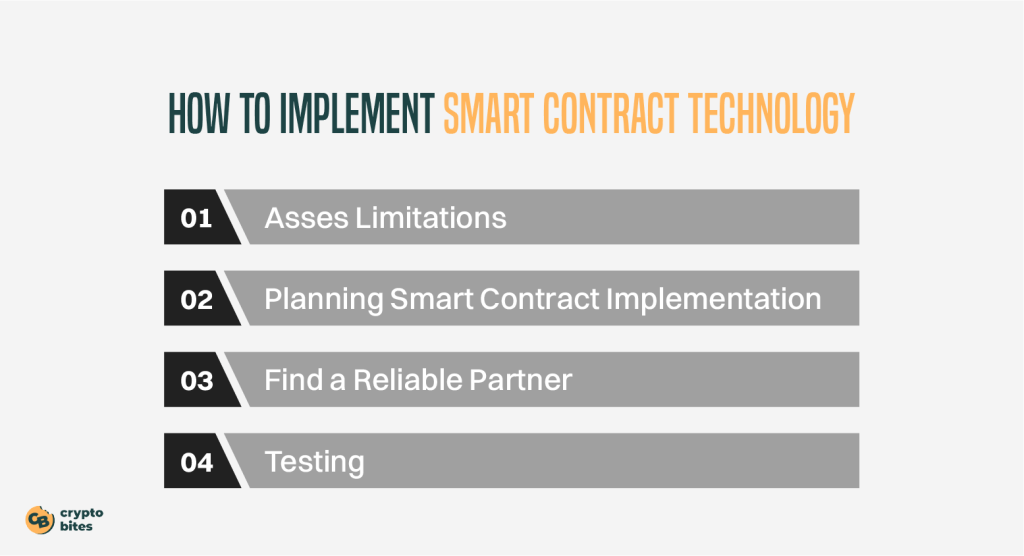

Here are four key steps that are usually followed during the implementation of smart contracts:

1. Asses Limitations

Keep in mind that smart contracts are hard to update and operate on “if-then” logic. Sophisticated variations may have limitations, so be aware of potential constraints.

2. Planning Smart Contract Implementation

Outline terms, conditions, and transaction handling in a detailed plan. Define actions under various conditions and establish rules for non-compliance. Create a clear roadmap for your smart contract implementation.

3. Find a Reliable Partner

Choose a smart contract creation company that understands your enterprise needs. Ensure they possess expertise in networks, consensus techniques, decentralized technologies, and other relevant tools to meet your requirements.

4. Testing

Before going live, conduct a thorough smart contract audit to identify and address potential bugs. Test the contract’s functionality with a few users, attempting various scenarios to verify its reliability and performance.

Decentralized Applications (DApps)

DApps are applications that run on a peer-to-peer network of computers, as opposed to a single computer. Leveraging the Ethereum blockchain, developers create these apps to offer various services, from games to finance, without any single point of control. The characteristics and benefits of DApps include:

- Open Source: They must be open for public scrutiny, which promotes a community-driven model of development.

- Decentralization: No single entity has control over the app’s data or operations.

- Incentive Layers: Most DApps have tokens to reward users and keep the network secure.

Blockchain in Business and Finance

Blockchain technology is revolutionizing the way you engage with the financial spectrum and manage supply chains. With its peer-to-peer structure and the emergence of decentralized finance, businesses across the globe are finding new ways to interact, trade, and secure transactions.

Decentralized Finance (DeFi)

In the realm of DeFi, you’re looking at a financial world where traditional middlemen such as banks and brokers are no longer necessary. Imagine having the ability to access financial services, including loans, insurance, and trading, directly from your peers. DeFi platforms operate on cryptocurrencies and smart contracts, offering you a secure and transparent ecosystem for your financial transactions. They enable you to partake in global financial markets from your digital wallet, making transactions faster and often more cost-effective.

- Peer-to-peer transactions: Direct transfer of assets, bypassing traditional institutions.

- Smart contracts: Automated enforceable agreements that do not require intermediaries.

Supply Chain Management

The integration of blockchain into supply chain management offers you an unprecedented level of transparency and traceability. From the moment a product is manufactured to the moment it lands in your hands, every step of its journey can be recorded and verified on a blockchain. This reduces the chances of fraud and errors, ensures the authenticity of products, and strengthens the entire business network. Whether you’re a supplier, manufacturer, or consumer, blockchain gives you a single source of truth that’s hard to dispute.

- Provenance tracking: Recorded history of all transactions associated with a product.

- Real-time visibility: Immediate insight into the location and condition of goods in transit.

What is a Consensus Mechanism in Blockchain?

A consensus mechanism is like a set of rules that a group of computers in a blockchain network follow to agree on which transactions are valid and the current state of the shared ledger. It ensures that everyone in the network reaches a common understanding, preventing issues like double-spending and maintaining the security of the decentralized system. Different blockchains use various consensus mechanisms, each with its own strengths and weaknesses, depending on the project’s goals.

Proof of Work vs. Proof of Stake

Proof of Work (PoW) was the original consensus algorithm in a blockchain network, notably used by Bitcoin. In this system, miners compete to solve complex mathematical puzzles with high-powered computers. When they solve the puzzle, they are permitted to add a new block to the blockchain and are rewarded with cryptocurrency. This process, known as mining, requires significant amounts of electrical energy.

- Pros of PoW:

- Security: PoW necessitates substantial computational power to manipulate the network.

- Decentralization: It allows for a competitive mining environment without the need for trust among miners.

- Cons of PoW:

- Energy Consumption: High energy requirements contribute to environmental concerns.

- Scaling Issues: The process can lead to slower transaction times during high network congestion.

On the other side, Proof of Stake (PoS) is seen as a greener and more energy-efficient alternative. Validators in a proof-of-stake (PoS) blockchain are chosen to create new blocks and verify transactions based on the amount of coins they own and are willing to “stake” as collateral. The higher the money or stake a validator has in the system, the greater their chances of being selected.

- Pros of PoS:

- Energy Efficiency: It greatly reduces the energy consumption by eliminating complex mathematical calculations.

- Faster Processing: It can process transactions quicker than PoW, leading to increased scalability.

- Cons of PoS:

- Potential Centralization: Wealth concentration could lead to a small group controlling the majority stake.

Other Consensus Algorithms

While PoW and PoS are the most prominent, several other consensus algorithms exist, each with unique features tailored for different blockchain applications.

- Delegated Proof of Stake (DPoS): Faster and more energy-efficient than PoW, DPoS allows token holders to vote for a few delegates responsible for achieving consensus and securing the network.

- Proof of Authority (PoA): Suited for permissioned networks, PoA designates approved accounts or nodes as validators based on their reputation, not their stake or computing power.

- Proof of Space (PoSpace) or Proof of Capacity (PoC): These require validators to allocate disk space rather than perform work or stake coins, aiming for a more egalitarian mining process.

By selecting the appropriate consensus mechanism aligned with your network’s goals, you can influence factors like security, speed, environmental impact, and the level of decentralization. Each mechanism balances these aspects differently, shaping the behavior and evolution of the blockchain it governs.

Blockchain and Identity Verification

When you think about verifying your identity, traditional methods like passports and driver’s licenses come to mind. But blockchain is changing the game, providing a way to manage your digital identity with enhanced security, privacy, and control over your personal credentials.

Blockchain for Digital Identity

Blockchain technology has become a pivotal innovation for your digital identity. It isn’t just a trend; it’s transforming the way you manage and present your credentials online. By encrypting and distributing your identity data across a network, blockchain reduces the risk of fraud and identity theft. Your identity information becomes a collection of verified digital records that you, and only you, can easily control and share.

- Privacy: Your personal data is protected, as blockchain enables you to share your identity without giving away sensitive information.

- Verification: Through mechanisms like hashing and consensus, blockchain can verify the authenticity of your credentials without the need for a central authority.

- Control: You hold the keys to your digital identity, metaphorically speaking, deciding who gets access to your personal records.

Real-World Blockchain Use Cases

In the real world, blockchain technology is not just a concept—it’s already operational. For instance, a platform by IBM leverages blockchain to facilitate auditable, traceable, and verifiable identity information. Imagine verifying university degrees or employment history in seconds instead of days.

Another practical application is in international travel. By using blockchain to verify your identity, you can look forward to potentially streamlining the process at border controls—making your travel experiences smoother.

- Educational Credentials: Digital certificates can be instantly verified, making the authentication of academic achievements more efficient.

- Healthcare Records: By controlling who has access to your health records, you can ensure that only the necessary parties view your sensitive health information.

As you can see, blockchain for identity verification opens up a world of possibilities while prioritizing your privacy and control over your personal data. But wait, there’s more to blockchain than meets the eye! From finance to healthcare and beyond, its uses are endless. Check out my blog for a deeper dive into the wild world of blockchain applications

Expansion of Blockchain

As blockchain technology grows, you’ll find its applications stretching far beyond the initial realm of cryptocurrency, influencing various facets of our digital and physical worlds.

Blockchain Beyond Cryptocurrency

The expansion of blockchain has accelerated its utility way past the confines of digital currency transactions. It’s transforming how you handle intellectual property by creating a transparent and immutable ledger for copyright and patent registrations. In the world of digital content, blockchain helps content creators to securely manage their digital rights, giving them more control and fair compensation for their work—changing the landscape of copyright management.

Interdisciplinary Applications

Blockchain’s versatility means it’s entering diverse domains, touching upon areas that directly affect you. In healthcare, it has the potential to overhaul how your medical records are stored, accessed, and shared, ensuring privacy and reducing the chance of errors.

Additionally, blockchain paves the way for peer-to-peer energy trading, allowing you to buy or sell excess renewable energy without the need for traditional intermediaries, which could democratize energy distribution. The implications for you are vast: you can expect increased control, efficiency, and reliability in these interdisciplinary applications as blockchain takes root.

By immersively integrating blockchain into these areas, the fabric of sectors like healthcare, intellectual property management, and energy distribution is poised to evolve, offering you more autonomy and security in your transactions and interactions.

Emerging Trends in Blockchain

The blockchain landscape is ever-evolving, and as you explore its depths, you’ll encounter recent innovations and ponder the future possibilities this technology holds.

Recent Innovations

Blockchain technology has excelled in creating Non-Fungible Tokens (NFTs), which have transformed digital art and ownership. With NFTs, artists and collectors benefit from a blockchain database that ensures the uniqueness and provenance of digital assets. Another significant advancement is the development of hybrid blockchains. These combine the best of both private and public blockchains, offering a flexible and customizable solution that enhances privacy while still maintaining a level of transparency.

- NFTs: A unique digital certificate registered in a blockchain that is used to record ownership of an asset such as an artwork or collectible.

- Hybrid Blockchains: Combines features of both private and public blockchains to offer controlled access and permission features along with maintaining the decentralized nature of the technology.

Check out more about hybrid blockchain here.

Role of Blockchain in Banking

Blockchain is poised to transform numerous areas, with one of the most significant being banking. Here is a detailed breakdown of how blockchain will shape our banking system in the future:

1. Blockchain in Auditing and Accounting

Blockchain technology is set to redefine auditing and accounting practices within the banking sector. With its unparalleled ability to maintain immutable data, blockchain streamlines traditional bookkeeping processes, providing a transparent and easily accessible record for audit purposes. Leading auditing firms, including PwC, KPMG, Ernst & Young, and Deloitte, are actively exploring its potential to enhance regulatory compliance in the financial industry.

2. Transforming Lending and Borrowing

Blockchain’s extensive verification capabilities have the potential to revolutionize lending and borrowing activities in banks. By mitigating the risk of bad loans and strengthening Know Your Customer (KYC) and Anti-Money Laundering (AML) processes, blockchain emerges as a crucial tool for risk management in the financial sector.

3. Streamlining Syndicated Loans

Blockchain offers a solution to the complexities associated with syndicated loans, where collaboration among multiple banks is essential. By automating and securing processes, blockchain addresses challenges related to KYC and AML compliance, significantly reducing administrative burdens and expediting loan approval timelines.

4. Digitizing Trade Finance

Trade finance, historically reliant on paper-based documentation, is poised for digital transformation through blockchain. This technology facilitates the digitization of trade finance, ensuring faster and more efficient transactions. Smart contracts on the blockchain automate and streamline various stages of trade finance, reducing delays and errors in the process.

5. The Impact on Trading Activities

The rise of decentralized finance (DeFi) signals a growing interest in decentralized marketplaces and exchanges, even beyond traditional banking. Blockchain’s potential to reshape clearing and settlement activities, critical components of the trading business, makes it an attractive option for enhancing transparency, security, and efficiency in the trading sector.

Wanna learn more about blockchain’s role in banking? Check out this complete guide.

What’s Nakamoto Coeffcient in a Blockchain?

The Nakamoto coefficient is a numerical metric designed to assess the decentralization level of a blockchain network. It measures the minimum number of nodes or validators required to compromise the network or execute a 51% attack. A 51% attack refers to a situation in which an entity gains control of more than half of the total computational power or hashing power on a blockchain network, allowing them to potentially manipulate transactions, double-spend coins, or disrupt the normal operation of the network.

In essence, the Nakamoto coefficient serves as a numerical indicator of the resilience and security of a blockchain system against centralization risks.

The higher the Nakamoto coefficient, the more decentralized and resistant the network is to attacks, as it signifies a larger number of nodes or validators that would need to be compromised for an adversary to gain control.

This metric is a valuable tool for assessing the robustness and security of blockchain networks in terms of their distributed nature and resistance to potential malicious actors.

What is a DAO?

A DAO, or decentralized autonomous organization, is a digital management structure governed by smart contracts, with decision-making processes recorded on a blockchain. Members participate in voting on the details of smart contracts that determine the DAO’s operations. This decentralized approach enhances transparency, eliminates the need for a central authority, and allows for more inclusive and democratic decision-making, making DAOs important in fostering decentralized governance in various sectors.

What is a Zero Knowledge Proof in Blockchain?

In the context of blockchain, a Zero-Knowledge Proof (ZKP) is a cryptographic technique employed to verify the authenticity of a statement or transaction without revealing any additional information other than the fact that the prover possesses specific knowledge. In a blockchain scenario, where transactions are recorded on a public ledger, the use of ZKP enhances privacy and security.

In a Zero-Knowledge Proof, a prover can convince a verifier that they have knowledge of a particular value without disclosing the details of that value. This is achieved through a process where the prover demonstrates knowledge of a secret, often referred to as a witness or private key, in a way that does not disclose the actual content of the secret.

For instance, consider a blockchain transaction where a user wants to prove ownership of a specific asset without revealing the details of their private key. By using a Zero-Knowledge Proof, the user can convince the network that they have the rightful ownership without exposing the sensitive information.

The key characteristics of Zero-Knowledge Proofs in blockchain include:

- Privacy: ZKPs allow parties involved in a transaction to maintain the confidentiality of their sensitive information. Only the validity of the statement is proven, and no additional details are disclosed.

- Authentication: ZKPs provide a means for one party (the prover) to authenticate themselves to another party (the verifier) without revealing any unnecessary information, thereby establishing trust in a transaction.

- Non-Interactive: Some ZKPs are designed to be non-interactive, meaning that the proof can be generated and verified without the need for continuous back-and-forth communication between the prover and verifier. This is particularly advantageous for efficiency in blockchain systems.

Zero-Knowledge Proofs play a crucial role in enhancing privacy and security in blockchain transactions by allowing participants to prove the validity of their statements without divulging unnecessary details, contributing to the overall confidentiality and integrity of the blockchain ecosystem.

What is Tokenization?

Tokenization in blockchain refers to the process of creating and managing digital tokens that represent ownership or rights to real-world assets on a blockchain network. This process involves converting physical or abstract assets, such as real estate, art, equities, bonds, intellectual property, identity, or data, into digital tokens that are recorded and secured on a blockchain.

Future of Blockchain

As you look ahead, the future of blockchain is vibrant and brimming with potential. Expect to see blockchain databases integrating with various industries outside of finance, from simplifying supply chain logistics to securing medical records. Furthermore, innovations within blockchain architectures aim to solve scalability issues, potentially paving the way for wide-scale adoption across multiple sectors.

- Scalability Solutions: Efforts are underway to increase blockchain’s capacity to handle a larger number of transactions which could lead to its widespread use in sectors such as healthcare and logistics.

- Industry Adoption: More industries are considering blockchain as a means to enhance security, transparency, and efficiency within their operations.

Frequently Asked Questions

In this section, you’ll find clear answers to some of the most frequently asked questions about blockchain technology.

What distinguishes a blockchain wallet from other types of digital wallets?

A blockchain wallet specifically interacts with blockchain networks to send and receive digital currencies, ensuring transactions are secure and immutable, unlike other digital wallets which primarily focus on simple payment and storage functions.

Could you highlight the main pros and cons of adopting blockchain technology?

Blockchain’s advantages include enhanced security, improved traceability, and increased efficiency and speed. Conversely, its limitations involve high energy consumption, complex integration with legacy systems, and regulatory uncertainty.

How is blockchain technology impacting the healthcare industry?

In healthcare, blockchain enhances data security, patient privacy, and enables the safe transfer of medical records, transforming how information is managed within the sector.

What are some common uses for blockchain technology outside of cryptocurrency?

Beyond digital currencies, blockchain serves in supply chain management, smart contracts, and even in verifying the authenticity of products. Learn more from this overview of blockchain uses.

Can you explain the basic concept of blockchain to a beginner?

Think of blockchain as a digital ledger that’s copied across multiple computers. Whenever a transaction occurs, everyone’s ledger updates. This collective validation creates a highly secure and transparent record-keeping system.

How does blockchain technology fundamentally work?

Blockchain operates on a distributed ledger system where each participant holds a copy of the transaction record. This ensures transparency, as changes require network consensus, making the data tamper-evident.